In our FinTech: The 2020’s blog post one of the areas we highlighted of particular interest was the “Financialization of Everything.” In it we noted that the youngest cohorts of Millennials & all of Gen Z have grown up in a world where everything from Sneakers to eSports virtual skins, to Trading Cards, can be bought and sold in some semblance of an exchange paradigm.

In our view there are really three predominant marketplace constructs that are optimal based on the underlying market and they include:

· Supply of One- Auction is the best format to optimize for price

· No Meaningful Supply Constraint- The seller “lifting” model is ideal (e.g., Amazon)

· Supply Constraint- Stock Marketplace is the most efficient model.

We think this is a trend that has been percolating for some time but has seen an acceleration as a result of COVID-19 for a variety of different reasons based on market verticals. Whether it’s the long tail of “alternative alternative” assets, venture-backed company shares, software contracts, or sport teams the financialization of everything is on its way. We take a look at some of the more conceptually interesting end-markets and companies that we’re tracking as these trends unfold in real time.

“Alternative Alternative” Assets

Post the passage of the JOBS Act in April of 2012, there was an expectation that we’d see a swell of companies take advantage of this in order to “democratize” capital formation. It led to the creation of Reg CF (which explicitly permitted crowdfunding), a modified & more useful version of Reg A, general solicitation for Reg D 506(c) offerings, while lowering the IPO registration burden for “emerging growth” companies. Parts of the legislation had proponents across Silicon Valley including people like Naval Ravikant as well as the NVCA itself. While there have been some Crowdfunding 1.0 platforms, most of them struggled to find product market fit. We’ve seen a generation of alternative asset marketplaces that have arisen over the past few years, allowing “access” to assets in both equity & physical form that are starting to show early signs of product market fit. For most of these assets there is some semblance of supply constraint so we believe a traditional “stock marketplace” format is the most efficient model of price discovery.

· Asset Class Agnostic- Given our view that most of these long tail of “Alternative Alternative” assets should trade in a marketplace construct we think the most successful companies will be those that are asset class agnostic. Right now the clear leader in this space is Rally, which initially offered the ability to invest in classic cars and has since expanded to sports memorabilia, watches, whisky / wine, comic books, hang bags, & literature. They have completed or are in process of completing 106 different offerings totaling ~$12.2mn. Otis is looking to compete with them and slightly earlier in their evolution as another diversified marketplace, at 26 offerings totaling ~$1.6mn. You also have a subset of sector specific markets that have started to see traction in Art with Masterworks, in horses with MyRacehorse & SportsBlx, and “pop-culture collectibles” with Mythic Markets.

· Art- The art market is estimated to be somewhere between $1.7-$2.0 trillion growing to $2.5-$3.0 trillion over the next five years. Deloitte did a survey of wealth managers and found that ~85% of managers believe the move towards a holistic wealth management model is an argument in support of including art & collectibles within this service and that 64% of managers surveyed were offering these services. Masterworks aggregates data to size the art market in their thesis for Art as an investment noting that UHNWI have a ~6% allocation to art as an asset class. They highlight that there is ~$67.5bn of annual sales, $31.0bn of which occurs at auction houses vs. ~$35 billion in annual sales. While art is one of those asset classes where some of the most desired works are a “supply of one” and therefore an auction format is optimal for price discovery, once these assets are sold, and fractionalized, there is support for them to trade in a stock marketplace construct. Due to the power of the auction houses & curators, despite its size & the turnover, art is one of the most opaque and least transparent markets riddled with intermediary fees and a lack of true price discovery. While this is in part, by design, if wealth managers are truly looking to include art as part of a holistic wealth management mandate we’ll need to see secondary liquidity. While some of the vertical dedicated platforms like Masterworks may carve out a niche in origination we think trading will emulate that of any other asset class which is sector agnostic on a platform such as Rally.

· Cars- According to IBISWorld from 2003-present the classic car market has seen ~$1.5-$2.0bn / year of transaction volume which means there’s $10’s of billions of dollars invested in cars as a “store of value” and / or investment opportunity. This was a market that was surprisingly early to make the migration online with collectors coalescing around websites like Bring A Trailer, which provide auctions for a variety of vehicles & a vibrant community that discusses these cars. Rally took the first step in creating securities out of these assets, and while it’s considerably smaller than the Art world given some of the non-correlated nature of these variety sub-asset classes within the long tail of “Alternative Alternatives” we think you’ll start to see increased interest from a portfolio allocation perspective.

· Collectibles- The estimated size of the global collectibles market is $370 billion and until recently this was largely physical in nature. We think you start to see not only continued growth of the legacy “collectible” market but new markets evolve that are natively digital. Boxes CEO Solomon Engel quotes over “200 million collectors” globally. There have been a number of marketplaces developed to cater to different parts of this market such as Mythic Markets, Vino Vest (wine), etc… While we think many of these individual cohorts are too small individually we believe again they will find product market fit as part of a broader platform. StockX has blazed the way here with Sneakers which they peg at a ~$6–$7 billion resale market & ~$100 billion global retail market. They’ve expanded into streetwear, collectibles, handbags, and watches all while raising at a $1.0bn+ valuation less than 3 years after launch.

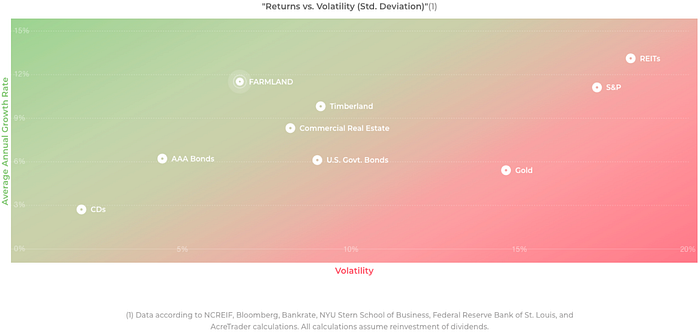

· Farmland- Land is one of the oldest investments globally and given the growth in global population, demand for food, and shrinking available acreage, it has become more & more attractive as an investable asset class. There has been no shortage of marketplaces launched in recent years to target this market including AcreTrader (which raised $5.0mn in a Series A), Growers Edge (which raised $40mn in a series B), and a handful of other non-venture backed companies such as FarmTogether, FarmFundR, and Harvest Returns. AcreTrader shows that the returns on farmland have been positive every year since 1990 and on a risk adjusted basis it outperformed all other assets (including Timberland, Commercial RE, and US Gov’t Bonds); with returns in line with the S&P despite significantly lower volatility. Farmland as an asset class has historically been inaccessible given the high minimums (often ranging in the millions of dollars), as well as cumbersome diligence process, filled with intermediaries. These platforms all serve to connect investors with curated properties and handle the structuring / diligence, and ongoing dialogue with the operator, etc… There is specialization & oversight required on the front-end, but we believe for secondary trading & distribution there are a number of different partnerships that could be cemented for the various platforms.

· Sports Teams- We have been vocal about the only way for the Big 3 (sorry NHL / MLS) sports leagues in the US (this is less of a problem internationally) to continue to grow in value, they will need to enable increased “financialization” by opening up access first to funds, and then allowing these assets to either trade publicly once again, or in a closed environment amongst a subset of pre-approved investors. There’s ~$220.0bn of aggregate enterprise value amongst the Big 4 US teams with <450 people in the world that have direct ownership (the ultimate scarcity value asset). Each of the leagues has started to take steps to look to support ever raising valuations with a dwindling number of billionaires in the world that 1) Can afford to buy a sports team that 2) Want to buy a sports team and 3) Don’t already own one. In the MLB they changed ownership rules to allow fund vehicles to own up to 14.9% of multiple teams. The NBA launched a vehicle alongside Dyal & Neuberger Berman to acquire LP stakes. The NFL is allowing owners to increase debt capacity from $250.0mn to $1.0bn after they were “disappointed” with the clearing price of the Carolina Panthers to David Tepper at “only” $2.2 billion. There are a number of first movers such as Sal Galatioto & Galatioto Sports Partners as well as Doc O’Connor and Arctos Capital looking to be first movers in this space. We even saw our first SPAC in the sector with none other than Billy Beane of Moneyball fame and Gerry Cardinale of Goldman Fame, targeting a $500mn vehicle for what they’re calling “RedBall Acquisition” You have PE firms like Silver Lake that have significantly increased their presence across the sports landscape with investments in companies like Endeavor, Fanatics, IMG, MSG, UFC, etc… We think you’ll see increased allocation from “institutional allocators” (e.g., Sovereigns / Pensions) that view this as a RE + Media + Royalty play that’s uncorrelated in nature; who by mandate need to take passive stakes. The leagues will look to maintain as much privacy as possible for negotiations vs. player’s unions / media partners, etc… but a permissioned closed-network of pre-approved investors may be the best of all worlds. For the long tail of other sports / teams / athlete monetization we think you’ll see a variety of platforms spin up that look to cater to that as an alternative to “gambling.”

· Ticketing- Existing Ticket Marketplaces such as StubHub / TicketMaster were built for brokers not end fans & this complacency from the powers that be have led to a lack of innovation, with the ticketing experience little changed over the past 15+ years. Mobile computing has given rise to a number of location based & real-time networks (e.g., Uber / Lyft, Bird, DoorDash, Postmates) but live events remain undisrupted. Ticket prices ultimately are inflated on the secondary market due to broker intermediaries hoarding inventory and the talent (e.g., teams / musicians / celebrities) never reaps the benefit of this. Given the “constrained supply” we think this is also best suited for a stock marketplace model. If done properly the talent can receive proceeds from secondary sales and with enough scale you can even disrupt the primary market. As a result of COVID-19 there’s real financial pressure on TicketMaster / StubHub and their respective ParentCo’s, which could provide the opportunity for a next generation company to attract talent to finally disuprt this industry which is $100B+ / year.

What’s Next: As we’ve seen a re-bundling trend of Neo Banks / Digital Wallets / Brokerage firms start to converge on product offerings with Bank Accounts, Equity Trading Functionality, Crypto Trading, PFM tools, etc… we think the next logical evolution of that is the addition of the long tail of Alternative Alternative assets for a retail crowd, and the higher end Alts for accredited investors +. There’s no reason the Square Cash App shouldn’t have your Bitcoin, next to your Apple stock, next to your Michael Jordan rookie card, next to your Banksy painting, and Mid-West Farmland, all in the same place, allowing for interoperability of funds to enable holistic portfolio allocation. We view some of these platforms transitioning from end-to-end marketplaces as “originators” of product while few such as Rally, becoming asset agnostic marketplaces and distribution partners into other FinTech platforms.

Alternative Assets- In the US there are ~$10-$12.0 trillion of investable assets held at RIA’s predominantly through two main channels: 1) Wirehouse Banks ($7.0 trillion) and 2) Regional RIA’S / Broker Dealers ($3.0-$5.0 trillion). While the average institutional investor might have a ~30–40% allocation to alternatives, the average individual at an RIA with assets at a Wirehouse bank on average have an ~8–10% allocation to alternative assets, while those at a Regional RIA have a ~1–2% allocation. There isn’t a difference is sophistication amongst financial advisors, or net worth of end-clients, however there is a big gap in “access” and infrastructure. “Alternatives” have historically been used as a catch all for all things not publicly listed including limited partnership interests in Hedge Funds, Private Equity Vehicles, and Venture Funds, single asset exposure to private companies, private credit, real estate, etc… There are a number of platforms leading the way here with different end offerings:

· Artivest / CAIS / iCapital- These platforms initially looked to “democratize” access to alternatives largely in the form of limited partnerships. They created master feeder fund structures reducing minimum check sizes down from $1-$5.0mn to $100,000-$500,000 and have since implemented parallel fund vehicles. They have successfully integrated with thousands of RIA’s representing trillions of investable assets. They are now providing services beyond just fund admin looking to slowly offer a broader suite of products including access to single assets. We think they have a unique position in the ecosystem with some of the most desirable “distribution” capabilities and should be viewed as potential partners for any of the institutional-grade “origination” platforms down the line for both single asset and fund vehicle structures.

· Cadre / CrowdStreet / PeerStreet- Real Estate has historically been viewed as its own asset class or as one of the largest allocations within alternatives so it’s no surprise that platforms that looked to democratize access to commercial real estate & real estate debt were among the first to get funded and gain market share. Since 2014 Cadre has completed $3.0bn+ in transaction value, with an 18.2% realized net IRR, and 1.5x realized net multiple value. CrowdStreet has passed $1.0bn in transaction volume across 80,000+ investors, 193 operators; including $511mn in 2019 alone. PeerStreet was the first two-sided marketplace focused on investing in real estate debt. They’ve been able to aggregate a nationwide network of private lenders / brokers on one side with individual & institutional investors on the other side. As of last year they surpassed $3.0bn in loan transactions and successfully raised a $60mn Series C coupled with $4.25 billion of new capital commitments; indicative of the pipeline investors believe they can source. While there are many people smarter to opine on the future of commercial real estate, RE will almost undoubtedly continue to be part of portfolio allocation and therefore institutional grade platforms such as these will have a place in the market.

· Carta / EquityZen / Forge / NPM / Zanbato- In 2015 private market capital raising surpassed public market capital raising for the first time, the average time from formation to IPO of a company has more than doubled over the past two decades, and despite a significant growth in AuM for asset managers there’s less companies to invest in publicly. Credit Suisse published a great piece on this in 1Q17 which is a bit dated but shows these trends, which have only accelerated since. There was a series of Generation 1.0 companies that tried to cater to this including SecondMarket (which became NASDAQ Private Markets) & SharesPost; which really took advantage of the hype around Facebook / Twitter when they were still private. A generation 1.5 came to be in Equidate (which became Forge) and EquityZen which created SPV’s and other structured products to invest in private company shares. Forge took it a step further (with greater regulatory risk) creating synthetic forward swaps with (and without) issuer approval. The next generation of private company exchanges are looking to automate a number of these manually intensive processes that permeate the ecosystem today. The default offering for nearly each of them is a tender offer solution, but we think a marketplace is the right construct if the operators / companies / investors look to concentrate liquidity periods.

Tribe Capital wrote a good piece on private markets discussing their recent Carta position. They write that:

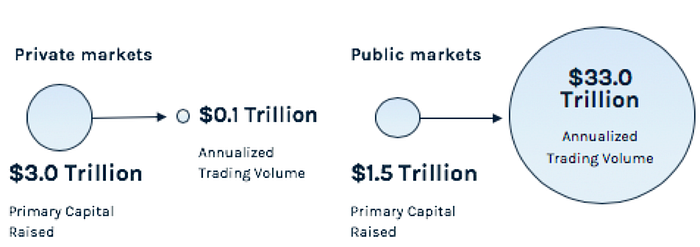

“There is a dire need to offer regular liquidity in the private markets to propel entrepreneurship. To put a number on the gap in liquidity that has emerged as companies stay private longer, consider the following.

About 2x as much primary capital is raised in private markets than in public markets. However trading volumes are fully 330x higher in the public markets, demonstrating an enormous gap in liquidity between the private and public markets.”

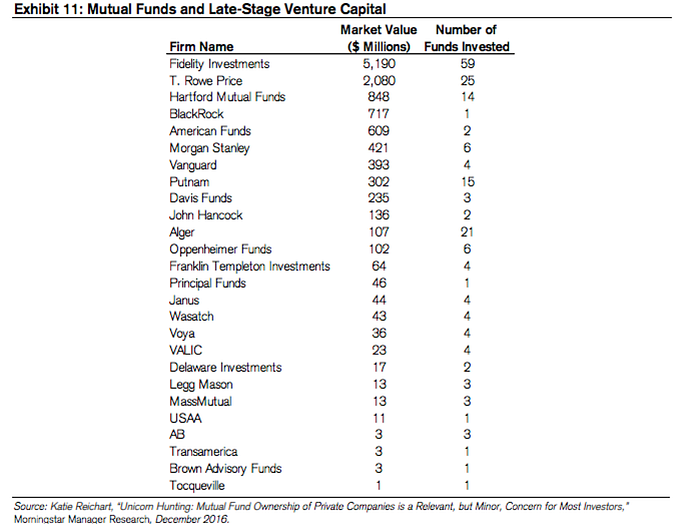

This becomes relevant as you have a number of “cross-over” funds not just Hedge Funds like Tiger & Coatue, but long only asset managers such as Fidelity, T. Rowe, and BlackRock. The head of global equity capital markets at Fidelity has suggested that “the pre-IPO market has become the IPO market of the past.”

· YieldStreet- LTD YieldStreet has placed $1.3bn+ of investment product on their platform with ~$350mn in real estate, ~$250mn in Marine, ~$65mn in Art, and $430mn in “other”. They typically offer high yielding (high single digit-low double digit yields) ABS products that are 6–30 months in duration.

What’s Next: As these platforms go from hundreds of millions of dollars of issuance a year to billions of dollars per year we believe there is a maturation process that will develop as it pertains to issuance, distribution, and secondary trading. Ultimately we see a significant opportunity for these Alternative Trading Systems (ATS’s) that have approval for unregistered securities to become a “listing” destination for each of these platforms to augment distribution. By enabling secondary liquidity these debt platforms can offer longer duration paper which will allow for recycling capital. Secondary liquidity for Limited Partnership interests has already led to a massive growth in “Secondary Funds” but we think this will continue to allow for different strategies & funding mechanisms for blank pools of capital, early deployment, and seasoned portfolios.

Other Areas to Watch

Outside of Alternative Assets and the various sub-asset classes that fall within it there’s a number of different end markets where we’re starting to see momentum that we believe will be part of the “financialization of everything.”

· Diamond’s- The Diamond industry is a $90bn/year market that’s illiquid, opaque, with high friction, a high requirement of trust, and surprisingly limited “financialization” to date. As Synthetic Diamond’s continue to look like the real thing there’s a camp that believes those will be used for jewelry (for the masses) and the predominant use of natural Diamonds will be as a reserve asset as there’s no other element that’s dense, small, deliverable & easily authenticated. In comparison to gold only ~1.0% of diamonds are held as an investment asset vs. 28% of gold with ~$1.5 trillion of Diamonds above ground vs. ~$9.0 trillion of gold. There are only 7 diamond mines with no new mines discovered in the past 20 years. We wrote about the push for an alternative store of value discussing Gold & BTC but there’s a camp that believes Diamonds fit that bill as well. Diamond Standard has tried to create an exchange venue with a standardized “Diamond Coin” alongside MIAX. They’ve seemingly overcomplicated the concept with digital tokens but we think you can see this added to a broader exchange venue with the proper regulatory oversight.

· HELOC’s- QE Infinity has resulted in homeowners’ equity reaching record-setting levels, with BlackKnight estimating that U.S. homeowners are sitting on $6.2 trillion in untapped home equity. As Baby Boomers & the Silent Generation lack the traditional financial wherewithal to support increased longevity, home equity lines of credit continue to be one of the assets that we expect to see enhanced financialization. Mike Cagney’s Figure has raised over $225 million to tackle this problem (amongst others) and has reportedly securitized several billion dollars of HELOC’s life to date. We don’t view these as businesses by themselves given the one time nature of these transactions, but a wedge for other alternative products.

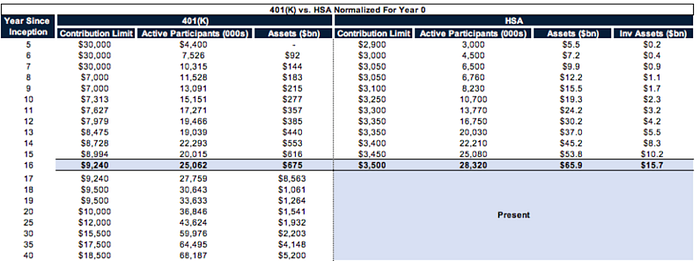

· HSA Accounts- HSA’s were established as part of the Medicare Prescription Drug, Improvement and Modernization Act, which was signed into law on December 8th, 2003. HSA’s are savings and investment accounts designed to help Americans with high-deductible health insurance plans save for their out-of-pocket medical expense. The biggest benefit is the fact that they are “triple-tax advantaged” allowing for 1) Pre-Tax Contributions 2) Tax-Free Earnings & 3) Tax-Free Withdrawals. They are portable and after the age of 65 you pay ordinary income but can use the capital for anything. Studies have found that ~60%+ of all bankruptcies are a result of medical problems & $300,000 is required on average at retirement for HC expenses with nearly ~1/3 of Americans unable to pay for that. It’s time for HSA accounts to be viewed in a similar vein to 401(K)’s & IRA’s and we’re starting to see some signs that that’s the case.

o HSAs now have ~$66bn in assets held over 28mn accounts which is +23% / 13% YoY respectively. 56% of accounts have been opened in the last 3 years. 37% of assets are held by accounts opened in the last 3 years. HSA investment assets reached $15.7bn in Dec ’19 up 54% YoY. On average investment account holders hold $16,012 total balance. This is the fastest growing sub-market within HSA’s. 24% of assets are in investments as of 12/31/19. There are now 1.2mn accounts investing a portion of their HSA +4.3% YoY.

o There are seven different Congressional proposals that would enhance HSA accounts including The Health Savings Account Expansion Act, and the Personal Health Investment Today Act of 2019. Collectively they would increase contribution limits, expand the types of expenditures allowed, while increasing the eligible universe of HSA account holders

o As we think about the modern worker ~80mn people don’t have access to employer benefits including freelancers, contractors, gig workers, founders, and full-time employees with inadequate benefits plans. Per IRS Data there are 10mn Full Time 1099s, 20mn 1099’s / W2’s & 50mn W2’s who don’t get benefits.

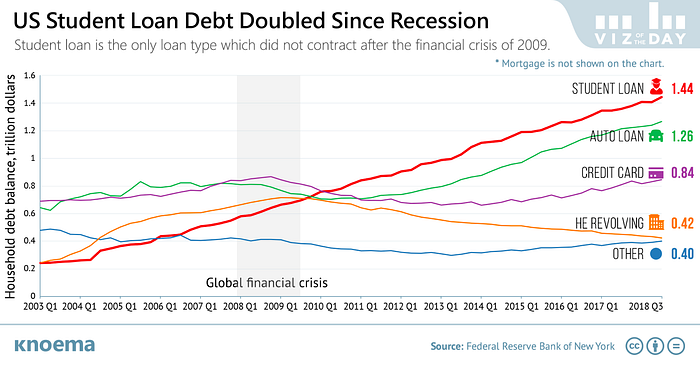

· Income Sharing Agreements- There’s ~$1.6 trillion in Federal & Private student loan debt outstanding across 44.7 million borrowers. This is not sustainable and will have a number of ripple effects down the line as it pertains to delaying home ownership, struggling to save for children’s education, all at the expense of retirement account growth, which puts further strain on benefits and healthcare expenses at end of life; perpetuating a vicious cycle. As people look for alternative methods of financing what’s old is new; income sharing agreements have gained some interest. An Income Sharing Agreement (ISA) is an arrangement where a student agrees to pay a fixed percentage of their income to their educational institution for a defined length of time in exchange for a waiver of some or all of tuition. While Milton Friedman was an early proponent of the idea in 1955, and Yale experimented with them in the 1970s (“Tuition Postponement Options”), during the past 5–10 years it has gained significant momentum in higher education in the US as an alternative to private student loans. There have been a number of platforms built looking to take advantage of this fledgling market. Purdue began partnering with Vemo Education to offer students ISA’s through it’s “Back a Boiler.” ISA Fund. They started with a $2 million fund, and since then have raised another $10.2 million and have issued 759 contracts totaling $9.5 million to students. Edly is looking to become “The ISA Marketplace” and they’ve developed a platform for schools, investors, and students to bridge the gap between schools & accredited investors who want to invest in ISA’s. While just starting they claim to have 16.6% return to investors thus far with 2,500+ students invested in. There’s clearly drawbacks to the model but we think we’ll see disruption in higher education financing one way or the other, which means new securities for investors to invest in.

· Middle Market Financing- Depending upon who you speak to it seems as if everyone has a different definition of “middle market.” There are roughly 200,000 companies in the US with revenues from $10 million to $1.0 billion most of which are closely held or family controlled. Such businesses produce roughly one-third of US GDP. Within the middle market universe, there are 32,000 private businesses with between $50 million and $1 billion in annual revenue, or about 16 times more than the number of equivalent public companies. Despite their size, history, and opportunity for operational efficiencies, they have much more limited funding options than public companies & “venture-backed” companies. As marketplaces begin to break down barriers between those that have capital & those that are in need of capital we believe middle market companies will be one of the biggest beneficiaries. Today Axial is the largest platform for buying, selling, advising, and financing middle market companies. We believe you’ll continue to see other platforms iterate on this concept and allow for direct negotiation as well as secondary trading.

· Patents- The patent industry is a $200bn+ market that is ripe for change given the convergence of technology & changing perception. The market is fragmented with hundreds of patent offices globally and discovery / intermediary costs average 30%+ which make transacting in smaller patents / patent portfolios (e.g., >$1.0mn) uneconomical. Patent financing is a ~$25 billion+ market & has grown in recent years with participation from PE firms like Fortress / Blackstone, etc…. As we start to see more exchange marketplace technology permeate different asset classes we believe the licensing & acquisition & financing of patents can be conducted through an exchange construct. IPwe is one of the first companies we’ve seen target this market & it looks like they have the domain expertise from a team perspective to execute on the stated vision. This could be lumped in with royalties more broadly but requires a differentiated skillset.

· Reward Points- The global Loyalty Program market was valued at ~$172.5 billion in 2018, with North America representing ~$72 billion. At any given point in time it’s rumored that AmEx reward points would be the #3 or #4 largest global currency, while SBUX has more mobile wallet users than almost any FinTech firm due to it’s loyalty program. Whether it’s credit card points, airline points, hospitality, or food & beverage these are assets that have been mismanaged for years. We believe we are in the early maturation of that and note there are several companies focused on that including NYSE / SBUX / MSFT portfolio company Bakkt. We’ve seen companies like Bumped look to offer reward points in the form of fractionalized equities. Ultimately if successfully executed we think an interoperable reward point system (for USD, equities, or even crypto) could be one of the next battleground areas for FinTech firms as it should represent a win / win for corporates & consumers.

· Royalties- According to the Encyclopedia Britannica the term royalty originated from the fact that in Great Britain for centuries gold & silver mines were the property of the crown; such “royal” metals could be mined only if a payment “royalty” were made to the crown. From non-renewable resource royalties to music, merchants, art, and software the royalty market is $100bn+ / year. In the music industry there are ~$2.5 billion of “Black Box Royalties” where you have publishers, writers, and artists who cannot be traced, with royalties never claimed. Spotify & Apple have to reserve for this as they don’t even know who they should pay. Depending upon the stage of development pharma royalties can be viewed analogous to software subscription revenue (more on that below) and may attract a differentiated investor base. The Royalty Exchange launched in 2016 and has passed $75 million in transactions life-to-date with $25.0mn in the past 12 months. They are playing way downstream with the average transaction price of $70,000. There have been funds raised that are dedicated to investing in film production with the goal of taking upfront risk for royalties on the back end, pharma royalties, music royalties, non-renewable resource royalties etc… As we start to see the institutionalization of this asset class, the ever growing demand for content, the strain on natural resources, and improved technology to track all of this we think they become yet another uncorrelated asset class that should warrant allocation.

· Software Subscription Revenue- In our piece This Time It’s Different: Maybe? we spoke about SaaS businesses and pointed to Robert Smith’s quote where he stated, “Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.” We elaborated on this concept breaking down software companies into “Central Nervous System” companies vs. “Appendix” companies; e.g., those that are critical for a business to operate & those that are a luxury. If you believe Smith & the stickiness of these contract, the companies should be able to borrow against this like any other asset on their balance sheet. Enter Pipe, which raised a $60 million seed extension from Tribe Capital, Fin VC, Anthemis, and existing investors Craft to create a marketplace for these SaaS companies to raise alternative capital besides taking on incremental equity dilution / debt. This will provide investors another way to express their view on the fundamentals of a given company, particularly when you are aware of factors such as Net Dollar Retention. Given the hundreds of billions of dollars of SaaS contract revenue outstanding, with the varying discounting to have access to that cash flow day one, we think this has the opportunity to be one of the single biggest marketplaces.

· Sports Gambling- Sell Side analysts expect the legal online sports gambling markets to grow from ~$430mn in 2018 to $26.0 billion over the next couple of years as legalization begins to take hold in multiple states. While global sports gamblers debate about the difference between European & American odds, we believe both are less than ideal as it pertains to scaled sports gambling. The ideal environment would be a continuous marketplace model with 0–100 probability (e.g., the old TradeSports) allowing two sided market participants, with the inclusion of HFT firms during events; with futures / forward pricing ahead of events. There’s no reason a robust spot market, forward market / options market cannot and will not arise for gambling. The US regulatory landscape is still incredibly fragmented on a state by state basis which would make pooling liquidity and a national exchange difficult (unless it somehow could fall under CFTC purview) but we believe we’ll see significant innovation in this area over the coming years.

If you’re an entrepreneur building a marketplace to facilitate the financialization of everything in any of the aforementioned areas, or something we missed; we’d love to hear from you.