FinTech continues to heat up with demand from both public & private investors & seemingly not enough supply. FinTech 1.0, 1.5.0, and 2.0 public companies have traded well over the past 12 months or enjoyed warm welcomes to the public market with companies such as PYPL +103.8% / SQ+188.7% / and ADYEN+107.5%. For the recent IPO’s AFRM is +102.9% since IPO, while LMND +414.7%. For the FinTech SPAC’s IPOE is +102.8% / and INAQ 49.7% +from trust value.

At the same time the global FinTech venture ecosystem has attracted over $40B of capital during the past 12 months across 2,450+ companies. This interest has occurred across various subsectors including Alternative Lending, B2B API Enabled Infrastructure, Capital Markets, Consumer Finance, Digital Assets, Financial Services, InsurTech, RegTech, and WealthTech; but no area has attracted capital quite like Payments.

Payments have long been the holy grail of “FinTech” even before it was referred to as such (e.g., Xoom, PayPal), and for good reason as global payments revenue hit ~$2.0T in 2019 and likely $1.9T in ’20 despite the COVID-19 pandemic per McKinsey’s latest report. While there are several markets that talk about their “TAM” in the trillions of dollars you’d be hard pressed to find many end markets generating that much in revenue.

The COVID-19 pandemic has had an impact on countless aspects of daily life, while in many ways serving as a societal accelerant pulling forward trends by years. The payments industry was no different with the ongoing shift towards digital payments, cash displacement (down 69% YoY), peer-to-peer payments, and growing eCommerce penetration. The pandemic has also accelerated the move from physical bank branches to natively digital banking; with banks closing branches and ATMs that won’t ever be re-opened. McKinsey notes:

“Overall, the crisis is compressing a half-decade’s worth of change into less than one year — and in areas that are typically slow to evolve: customer behavior, economic models, and payments operating models.”

There are a number of key macro factors converging for the payments industry providing both cyclical & secular tailwinds as we enter 2021. This makes the public company pure plays (FIS, FISV, GPN, MA, V) attractive from a risk / reward perspective, as they serve as a natural inflation hedge, have low capital intensity, have idiosyncratic margin expansion opportunities and are highly free cash flow generative. This also continues to result in a conducive funding environment for private companies.

Some of these trends include:

B2B / Corporate Payments- The B2B payments industry is projected at ~$125T; with accounts payable payments representing ~$110T of which ~20% is “card-able” and ~$10T is cross-border. Right now, ACH, Cash & Check represent ~$122T of that $125T market opportunity. The card networks have tried to be enablers by offering bill-pay, virtual cards, push payments, account-to-account technology but it’s not the payments that are an issue, rather antiquated processes of manual reconciliation given limited automation that make this process error prone. There are B2B pure-play companies such as FleetCor & WEX that are looking to solve this pain point. Virtual Cards have become a key proponent of the workflow here and are one of the fastest growing segments growing at ~4.0x the rate of the overall payments market. Given the difficulty with cash / checks in 2020 businesses have been forced to upgrade their back office / reconciliation process.

Cash-to-Card Conversion- COVID-19 has already led to a further decline in cash usage. This process had been well underway in the developed world but now Emerging Markets are also following suit. Visa through Visa Direct & Mastercard through Mastercard Send have made big strides in the “push-to-card” segment allowing for “instant” funding serving as a dynamic alternative to ACH. The pandemic has also accelerated the move towards contactless payments; which is replacing cash in small ticket items. The card networks net revenue yield could be more than ~2x higher on small-ticket transactions. The pandemic resulted in an acceleration of the contactless rollout forcing many merchants to upgrade hardware / card issuance over the course of the year now in excess of ~50%+ of cards in network.

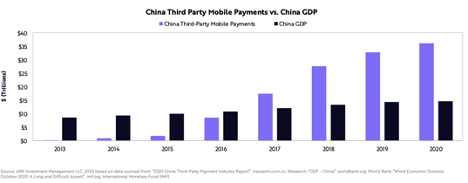

Digital Wallet Growth- In China mobile payments have exploded more than 15x in five years, from roughly $2T in 2015 to an estimated $36T in ’20; nearly 3.0x China’s GDP. This has now become a global phenomenon with leading digital wallet providers across North & South America, Europe, and Africa; following Asia’s lead. Cash App & Venmo have amassed 60M active users in the last 7 & 10 years respectively; this took JPM more than 30 years & 5 mergers to achieve. As the active user numbers grow, and these digital wallets serve as the primary bank account / financial partner for their customers; this too will result in an increase in mobile payment volume. Notably much of the activity is still routed via the card network rails.

eCommerce Acceleration- The global eCommerce market hit $3.9T in 2020. We’re seeing growth in eCommerce marketplaces ex-AMZN, ride-sharing, food delivery, subscriptions, video games, and general retail sales. Areas such as online travel / ticketing have faced headwinds last year but as we look to reopening in mid-21 should serve as beneficiaries from pent-up consumer demand.

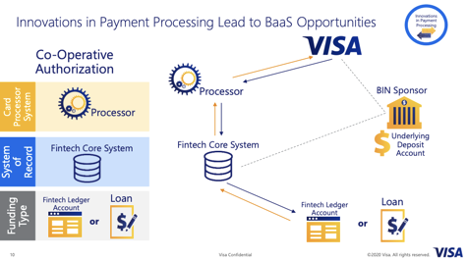

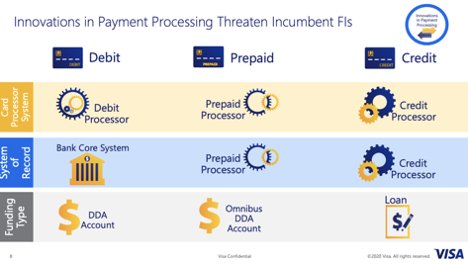

Embedded Finance- Visa discussed Banking as a Service (BaaS) & market trends & implications. They defined Embedded Finance as “non-financial companies that have value propositions that are significantly enhanced or even transformed through the associated financial products and services embedded within.” Quoting Matt Harris & Bain Capital they assume that ~40% of payments industry will move to the embedded model with ~$1.0T of market cap potential. They also highlight innovations in payment processing that in their mind threaten the incumbent FI’s.

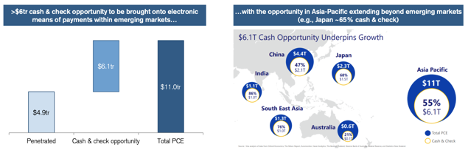

Emerging Markets- Emerging Markets have been seen as a key growth lever for payment companies expecting to growth at a 10%+ CAGR. Despite the growth in digital payments in China, Asia-Pacific is still ~50% cash & check. There have been active government initiatives to reduce cash in areas such as India & Japan. In areas such as Africa / LatAm there is increasingly high smart-phone penetration & in turn digital wallets. Credit Suisse estimates a ~$6.0T + opportunity.

Open Banking- The rise of Open Banking which allows for consented access to customer financial data has resulted in the demand for many of the FinTech products that exist today. B2B API infrastructure companies such as Plaid, Yodlee, Tink, and TrueLayer have led to the creation of new platforms from which these digital wallets / neo banks are built upon. This has resulted in new product creation with companies able to pick the highest value added products for their customers which often start with payments.

The broader macro trends discussed have had ramifications on all of the various subsectors that are payments & payments related including:

Payment Networks- Visa / Mastercard

Merchant Acquirers / Service Providers

o Payfac Enablers- Finix / Flow / Flutterwave

o IPOS- Revel / ShopKeep

o ISO / Acquirers/PSPs- Stripe

Bank Technology Partners

o Core Processers- FIS / FISV / JKHY

o BaaS- Moov, Rize, Unit

o Other Services- nCino, Treasury Prime

B2B Payments Networks

o AP/AR-AvidExchange

o Corp Cards & Expense- Brex / Divvy

o Cross Border- CurrencyCloud

o Instant Payments- PayFi

o Payroll- Gusto

Issuer Processing- Galileo / Marqeta / Stripe Issuing

Remittance- Remittly / Transferwise

C2B & P2P- Square, PayPal, Dwolla

Venture Funding

Given these macro tailwinds the venture ecosystem has been incredibly active; with a number of prominent raises over the past few months in the payments space. These raises have been occurring at earlier & earlier stages in the company’s lifecycle & ever-increasing valuations; which on a relative basis make some of the public incumbents look cheap comparably.

While there’s an overarching narrative that they will come & disrupt the legacy players the truth is much more nuanced. Almost all of the companies continue to run on V/MA rails with the exception of those focused on the ACH space. While companies like Adyen, Braintree (PayPal), and Stripe all compete with the likes of FIS, FISV & GPN for acquiring platforms & the goal to scale beyond just payments; the payments industry is too big for any one of them to own in totality.

· Stripe- Bloomberg reported that Stripe was looking to raise capital at a $70-$100B valuation. In April they raised an $850M Series G at a $36B valuation.

o In the September ’19 announcement Stripe said it processes “hundreds of billions of dollars.” Stripes standard structure is 2.9% + $0.30 per successful payment. Their margins are likely in the 50%+ range. They also have Stripe Atlas, Stripe Capital, a Corporate Card / Lending product but let’s round that to $0 for now. Assume they grew ~75% YoY from a $200B base; they would have processed ~$350B in volume last year. At a 2.9% rate that’s $10B in revenue. The average online order is ~$85, assuming that’s the average Stripe order that would equate to ~4B transactions; at a $0.30 per transaction fee that would generate another $1.2B in top line revenue, totaling ~$11.2B. This would be the total “gross” revenue applicable which would subsequently net out interchange + scheme fees, etc….

· Checkout.Com- Checkout.com raised a $450M Series C at a $15.0B valuation. This comes after a $150M Series B raise in June ’20 and $230M Series A in May ’19.

o The CEO mentioned they believe the will grow 80% at least in ’21 & tripled payment processing volume in ’20 vs. ’19. They generate “double-digit” millions of EBITDA.

· Klarna- Klarna raised a $650M round at a $10.65B valuation.

o Klarna is a BNPL company similar to AFRM & ADYEN. They claim to have 90M customers, including 9M in the US & is looking to go direct to consumer as well. As of late last year, their standalone app has ~12M MAU and 55,000 daily downloads. They were working with 200,000+ retail partners & generated $466M in revenue during 1h20 ($59.8M in losses) so likely ~$1.0B+ for FY20 in revenue.

· Marqeta- Marqeta is said to target a $10B IPO in 1H21; working with GS & JPM on the listing this comes after raising $150M at a $4.3B valuation last May.

o Marqeta allows companies to instantly issue & process card payments & has notable clients such as Uber, Square, Instacart. More recently they’ve partnered with incumbent FI’s such as JPM & GS on card initiatives. In 2019 Marqeta was said to do ~$300M in revenue lets assume they grew 100% YoY in ’20 it would be $600M + another 75% in ’21 it would put them on track for just over $1.05B.

· Melio- Melio raised $110M Series C2 at a $1.3B valuation led by Coature. This follows $130M raise last year and brings the total capital raised to $256M in just over 2 years since launching.

o Melio is targeting the B2B payment space; specifically enabling SMBs to pay customers electronically sing bank transfers, debt or credit card, along with paper checks if needed. Out of the ~$25T B2B wholesale payments industry paper checks are largely the predominant method, COVID-19 has accelerated the need for digitization & Melio reduced users paper checks by ~50% in ’20 vs. the 4–8% decline between ’03-’18.

· Fast- Fast raised a $102M Series B round led by Addition & Stripe after a $20M Series A in March ’20 and a $2.5M pre-seed round in October of ’19.

o Fast’s one-click purchasing process launched in September of ’20 allowing any eCommerce company to have an AMZN one-click check out experience. With three months of data and the number of merchants onboarded, it would be tough for them to have generated much more than a few $M in revenue. Raising $102M would likely put them at a $400-$500M post-money valuation; showing the demand for a product that can capitalize on that eCommerce wedge.

· Alma- Alma raised a $59.4M Series B alongside a $25.5M credit line.

o Alma offers BNPL capabilities for luxury goods in France. In France debit cards have much greater market share than credit cards. They believe they will hit €1 billion in annual payment volume within two years.

· Modern Treasury- Modern Treasury raised a $38M Series B round led by Altimeter Capital. More than $125T B2B payments are transacted globally between Cash / Check ($38T), ACH ($84T), and Cards ($2T). In the US ~88% of those are conducted via wires, checks & ACH payments which Modern Treasury is building workflows to cater to.

o They grew from $100M to $1.0B in reconciled volume over the past year. They charge bps on a % moved but likely single digit millions in revenue.

Venture M&A / Public to Private M&A

· Plaid / Visa ($5.3B)

· Galileo / SoFi ($1.2B)

· Finicity / Mastercard ($935M)

· SendWave / WorldRemit ($500M)

· Paystack/ Stripe ($200M)

Payments consolidation isn’t limited to the private markets as the incumbent public payment companies have been some of the most acquisitive over time. At the end of last year you also had conversations break down between FIS / GPN in a deal that would have been valued at ~$70B. The deal would’ve bolstered FIS’s merchant-facing business which currently accounts for ~20% of revenue.

· Worldpay / FIS- FIS acquired Worldpay for ~$35B as a means to expand its merchant business & geographic footprint.

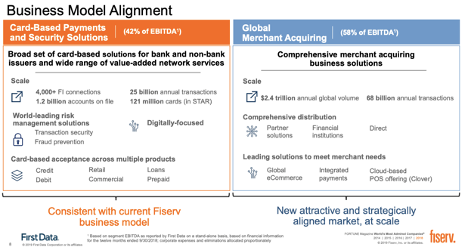

· First Data / FISV- Fiserv acquired FDC for ~$22B in order to offer a more comprehensive solution including an end-to-end payments platform from issuance to acceptance.

· Total Systems Services / GPN- GPN acquired TSYS for $22B as a means to expand its eCommerce presence.

The Industry Bellwethers

When looking at the payments landscape there’s a notable multiple discrepancy between V / MA & everyone else and for good reason. We’ve written numerous times that V & MA are two of the best businesses ever built, serving effectively as a tax or royalty on global commerce. They have incredibly high barriers to entry, attractive unit economics, and both cyclical & secular tailwinds. If you look at the types of companies that are receiving venture funding at present & that have scaled few have the ability to disrupt V / MA in their core business; while the companies continue to innovate & partner with FinTech firms to build on their rails. They are becoming the equivalent of “mission critical” software to the FinTech industry.

Visa (V)

The best write up on V came from the DOJ in their lawsuit to block the $5.3B Plaid transaction. A few excerpts:

· Visa is a monopolist in online debit transactions, extracting billions of dollars in fees annually from merchants and consumers.

· Visa is “everywhere you want to be.” Its debit cards are accepted by the vast majority of U.S. merchants, and it controls approximately 70% of the online debit transactions market.

· Because of its ubiquity among consumers, merchants have no choice but to accept Visa debit despite perennial complaints about the high cost of Visa’s debit service

· Visa’s monopoly power in online debit is protected by significant barriers to entry and expansion. Visa connects millions of merchants to hundreds of millions of consumers in the United States. New challengers to Visa’s monopoly would thus face a chicken-and-egg quandary, needing connections with millions of consumers to attract thousands of merchants and needing thousands of merchants to attract millions of consumers

· Visa has long-term contracts with many of the nation’s largest banks that restrict these banks’ ability to issue Mastercard debit cards. Visa also has hamstrung smaller rivals by either erecting technical barriers or entering into restrictive agreements that prevent rivals from growing their share in online debit, or both.

Visa’s ubiquity needs little explanation. During FY20 V saw 204B payments & cash transactions equating to 559M transactions per day, out of those 204B total transactions; 141B were processed by V. They have 145,400 financial institution clients & during FY20 their total payment & cash volume were $11.3T while 3.5B credentials were available worldwide to be used at nearly ~70M merchant locations. The DOJ’s point about any competitor facing a chicken-and-egg quandary is spot on; it’s incredibly difficult for any firm to bootstrap those network effects today.

Visa has not sat still on the move to digital payments & is focused on their “network of networks” strategy to enable money anywhere at anytime by facility P2P, B2C, B2B, SMB payments & G2C (government-to-consumer) payments. Visa calls this “new flows” and believes it represents a ~$185T market opportunity.

It’s not just their payments capabilities but the other value-added services that they offer their clients including issuer and consumer solutions, merchant and acquirer solutions, fraud management and security services, data products, and consulting and analytics. If data is the new oil it’s tough for anybody to compete with the sheer amount of data available to V on a daily basis to detect things like fraud.

Mastercard (MA)

While the DOJ complaint made it seem as if even MA wasn’t truly a V competitor; that was in part theatrics in terms of how they tried to define the end-market as “online debit services” to paint their antitrust picture. While the smaller of the two MA too enjoys ubiquity with 2.8B Mastercard & Maestro branded cars issued. Over the past 5 years as MA has gained market share & leaned in with FinTech companies it’s actually outperformed by ~75%. Both have handedly outperformed the S&P 500 while MA has also outperformed the NASDAQ.

Not surprising MA is a beneficiary of the same macro & micro trends as V with a similar product roadmap. MA discussed their focus on the secular shift to digital payments, real-time payments & open banking. They are focused on their “multi-rail flows” with growth from:

· PCE growth

· Cash to Card conversion

· Increasing Market Share

· Value Added Services

In 2019 MA delivered their “click to pay” activation enabling for a faster, more secure checkout experience across the web. They announced Mastercard Track which enables B2B payments by offering an open-loop commercial service. They have also been focused on P2P, B2C, and government disbursements.

The Unloved Incumbents

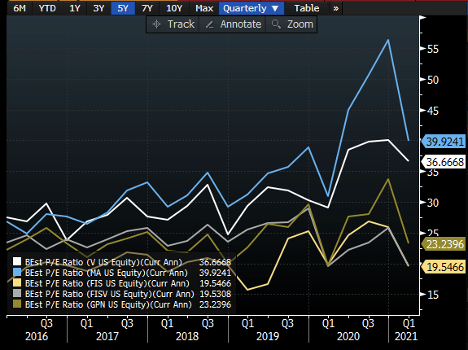

Although V & MA saw multiples expand in ’20 as the market was willing to “look through” the GDP shock, FIS, FISV, and GPN saw much smaller multiple re-ratings. While the core businesses have less sensitivity to GDP growth, they are still trading roughly in line with historical averages despite a broader market re-rating & strong cyclical & secular tailwinds for their core businesses.

While we have focused mostly on the potential disruption & innovation from challengers, the leading incumbents benefit from those same strong industry tailwinds coupled with M&A synergies that should make them some of the most attractive names to benefit from the re-open trade; with near-term competitive concerns overblown.

Fidelity National Information Services (FIS)

FIS is a leading provider of technology solutions for merchants, banks, and capital markets firms globally with solutions spanning merchant acquiring, integrated payment solutions, global eCommerce solutions, core processing and ancillary applications solutions, digital solutions, including internet, mobile and eBanking, fraud, risk management and compliance solutions, electronic funds transfer and network services solutions, card and retail payment solutions, wealth and retirement solutions, item processing and output services solutions, securities processing and finance solutions, global trading solutions, asset management and insurance solutions, and corporate liquidity solutions.

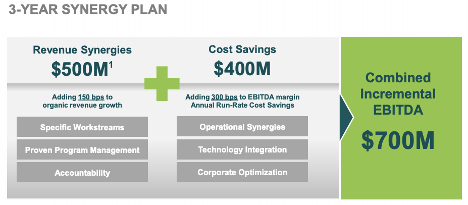

In July of ’19 FIS closed a ~$43B acquisition of Worldpay; which is a leader in eCommerce & payments that processes over 40B transactions annually, supporting more than 300 payment types across 120 currencies. As part of the merger, they guided to $500M of revenue synergies, $400M of cost savings, leading to $700M in EBITDA synergies.

We’re ~18 months post close and both FIS / Worldpay have done a great job not only hitting but exceeding synergy targets over the past 10 years with their largest acquisitions.

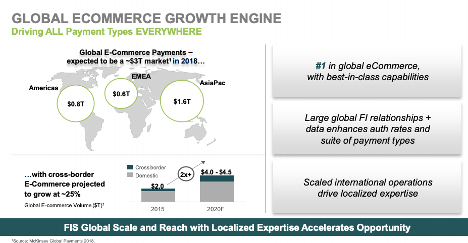

FIS is well positioned in eCommerce with deep online payments expertise allowing clients to buy anything, anywhere in any currency. They have access to unique world auth rates & fraud rates given relationships with 45 of the top 50 FI’s globally. This business is likely processing ~$400-$500B of eCommerce volumes / year in excess of Adyen, Braintree/PYPL, & Stripe.

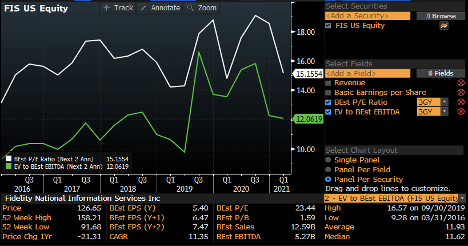

FIS currently trades at ~19.5x ‘21E EPS & 16.9x ‘22E EPS and is in-line wit it’s trailing 5-year forward multiple. This despite greater scale from the Worldpay merger, and a market re-rating which has the S&P trading at ~23.0x earnings.

There’s likely upside to these estimates as we see pent up consumer demand in 2H21 & the team outperforms their synergy guidance. It’s down ~14.5% over the past 12 months while the forward two-year outlook has arguably never looked more attractive from a company specific / macro convergence perspective.

Fiserv (FISV)

Fiserv is one of the largest third-party payment processors/merchant acquirers and providers of account processing systems; electronic payments processing products and services, such as electronic bill payment and presentment services, account-to-account transfers, person-to-person payments, debit network solutions, debit card processing and services, general purpose credit, retail private label and commercial credit card processing and services, and payments infrastructure services; internet and mobile banking systems; and related services, including card and print personalization services, item processing and source capture services, loan origination and servicing products, stored value network solutions and fraud and risk management products and services. They have three core businesses including (i) Acceptance (ii) Payment & Networks & (iii) FinTech

FISV started the recent wave of public M&A mega mergers between merchant acquirer/payment processing when it announced it was buying First Data (FDC) in Jan 2019 for $39B in cash, that deal closed in July of ’19. The acquisition was complementary to legacy FISV as it gave the company exposure to the merchant acquiring and credit processing space.

The acquisition of First Data provided them exposure to the faster growing merchant acquiring system. FDC was burdened with a high debt load after being LBO’ed by KKR in ’07 & like most PE companies in high growth industries lost share to challengers. There was room for margin improvement (which finally got back to ’07 levels in ’19) as well as organic growth opportunities. FDC was processing more than 93B transactions annually, had more than 1B card accounts on file, more than $2.4T of global payment volume for more than 6M businesses.

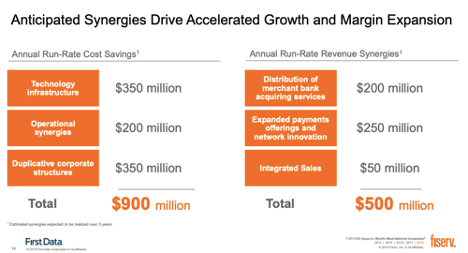

The companies guided to ~$900M of annual run-rate cost savings & $500M of annual run-rate revenue synergies leading to ~$1.1B in annual operating income synergies & ~$900M in FCF synergies. This provides ample liquidity to (i) Invest in R&D & (ii) Be acquisitive of potentially competitive upstarts.

Outside of the FDC acquisition they own the cloud-based Clover PoS operating system which serves ~6M businesses globally. They also own the third largest debit network behind V / MA & have exposure to the Zelle P2P network (which is just behind Cash App / Venmo) where they offer a turnkey implementation of Zelle by providing interface, risk management, altering, settlement & other services.

FISV is trading at near the lowest relative valuation to the S&P in ~10 years on both a P/E and EV/EBITDA basis & looks cheap to its own recent history; despite these tailwinds.

Global Payments (GPN)

GPN is the leading pure play payments technology company providing payments & software solutions to ~3.5M merchant locations and more than 1,300 FI’s globally. They have their Merchant Solutions segment which provide payment technology & software solutions to their customers & their Issuer Solutions Segment which provides solutions to enable FI’s to manage their card portfolios.

Global Payments announced the last mega deal of 2019 when they merged with TSYS to create a pro-forma company with a leading position in integrated payments, owned software in both merchant and issuing, increased scale in eCommerce and omnichannel solutions and further exposure to faster growth geographies and digital payment trends. Combined the companies offered payments & software solutions to ~3.5M SMB merchant locations and more than 1,300 FI’s across 100 countries. PF ~68% of revenue is from merchant solutions, ~22% from issuer solutions, and ~10% from consumer solutions.

They guided to ~$300M annualized run-rate cost synergies & ~$100M in revenue synergies; with expectations of realization by the end of year 3.

They are now at the half way point of merger integration and trade at a slight premium to FISV / FIS but still in line with recent history & a discount to the broader market.

Bottom Line:

There’s a ton of exciting innovation going on in the payment’s ecosystem by both public & private companies. The large cap public companies have lagged the market over the past 12 months & should benefit from a number of macro catalysts including cash to card conversion, eCommerce growth, and reopening benefits, coupled with a number of company specific catalysts.

We will likely see a handful more of these private companies enter the public markets this year & undoubtedly see more funding announcements.

The payments industry historically has been one of the most acquisitive industries over time & we expect to see this continue in both the public / private markets.