Background

If you rewind the clock ~100 years, prior to the Great Depression there was no concept of “public” or “private” markets; investments were on a continuum of liquid vs. illiquid and regulated vs. non-regulated. Like most things in 2020 the “ideal state” isn’t one of 100 years ago, yet in this instance it’s important to look at what changed and why.

The Wall Street Crash of 1929, also known as the Great Crash saw a two-day decline in the Dow Jones of 23% between October 28–29th, and ultimately resulted in the loss of 89.2% of its value in less than a three year period, bottoming in mid-1932. The reaction to the crash was to establish the Pecora Committee which was an inquiry begun by the Senate Committee on Banking & Currency to investigate the cause of the crash. This ultimately led the passage of Glass Steagall (which was in place until 1999 when it was repealed) and the Securities Act of 1933 and the Securities Act of 1934 which still govern the bulk of securities regulation today.

The ’33 Act has two basic objectives:

· Requires that investors receive financial and other significant information concerning securities being offered for public sale; and

· Prohibit deceit, misrepresentations, and other fraud in the sale of securities

While the ’34 Act created the SEC and empowered the SEC with broad authority over all aspects of the securities industry; including the power to “register, regulate, and oversee brokerage firms, transfer agents, and clearing agencies as well as the nation’s securities self-regulatory organizations (SROs)…. the Act also identifies and prohibits certain types of conduct in the markets and provides the Commission with disciplinary powers over regulated entities and persons associated with them. The Act also empowers the SEC to require periodic reporting of information by companies with publicly traded securities.”

The SEC has a list of “laws” that govern the securities industry today which includes eight different acts, five of which (62.5%), were developed in 1940 or earlier. So while it’s never a good idea to just rewind the clock 100 years, for the most part the current regulatory paradigm we operate in is the result of legislation passed between 80–90 years ago; with minimal amendments along the way.

As is the case when regulation is “stale” across any industry, market forces begin to coalesce around a more ideal end-state within the confines of existing rules forcing regulators to react. This is occurring today with the blurring of public & private investing as a result of a variety of factors including liquidity for private company shares, cross-over funds, SPAC’s, and the financialization of new asset classes.

Institutionalization of LP’s

In a recent blog post entitled Capital Allocation & Risk Asset Ramifications in a 0% Interest Rate World, we discussed the significant inflows into Hedge Funds, VC Firms, and Buyout Funds over the past 45 years with assets up 470 times over that period of time.

This has resulted in the “institutionalization of the LP” community where capital allocators have a variety of “strategies” through which they have investment committee approval to allocate to managers in that respective strategy. This has given rise to the consultant community, and in our opinion the hyper “specialization” of investors, forcing strategies to sit within these narrowly defined constraints.

On an episode of Pat O’Shaunessy’s Invest like the Best Podcast, Brad Gerstner the founder of Altimeter had a great quote about this phenomenon.

Brad starts off by saying when he founded Altimeter he was in Boston and there were a few great investors he spent time talking to including, Seth Klarman (Baupost), David Abrams (Abrams Capital), Paul Reeder (PAR Capital), who we’re running what he called “throwback funds” that looked like Buffett’s original hedge fund. He said “If you asked Buffett back in 1965 why did you invest in a private company out of your hedge fund? He would say, “Well, I invest in good companies. I just go and try to find the best investments. My LP’s get a pro rata share of all my best ideas and some of them are public and some of them are private.” And he clearly still runs Berkshire that way today.

Brad goes on to say if you look at the evolution of institutional investing it was LP’s who “pushed the investment firms into specialization. We want the best at Venture, the best at mid-stage private equity, the best at late-stage PE, the best at this type of hedge fund, absolute return, macro, etc… So investors started to force themselves into formulas, that for me, didn’t look particularly interesting, looked very difficult to generate meaningful alpha over a long period of time, and certainly didn’t optimize my happiness.”

Brad also discussed a slide he presented to his LP six years ago that identified three reasons as to why value was disproportionately accruing in private markets including:

· You have platforms that allow companies to scale faster (e.g., AWS, GCP, Azure) and in a more capital efficient way. With every successive generation the winners scale faster, in a more capital efficient manner.

· You have information advantages. There is less competition. If you are a lifecycle investor & invest from the period of time the company is worth $200M to $20B; if you are Fidelity and T Rowe and you want to participate in all of that value creation you cannot afford to not be in the private market.

· Venture does not allow you to sell.

IPO Market / Crossover Funds / SPAC’s

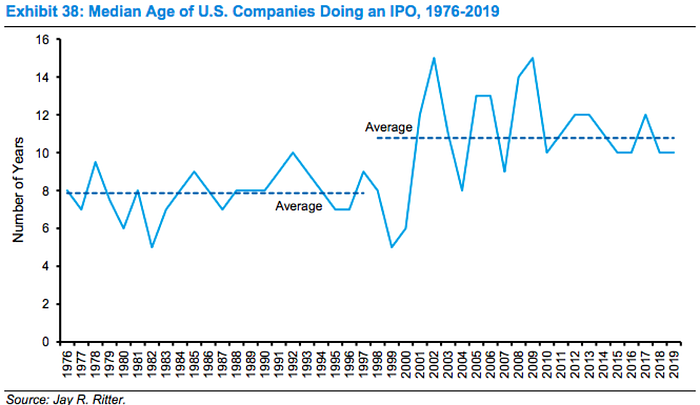

In a recent Morgan Stanley report entitled Public to Private Equity in the United States: A Long-Term Look, they looked at the age of a company during an IPO which has risen from a median age of 7.9 years from 1976–1998 to 10.8 years from 1998 to 2019; a 37% increase. If you extend the first period through the dot-com boom, the median age has increased closer to 50% from 1976–2000 to 2001–2019.

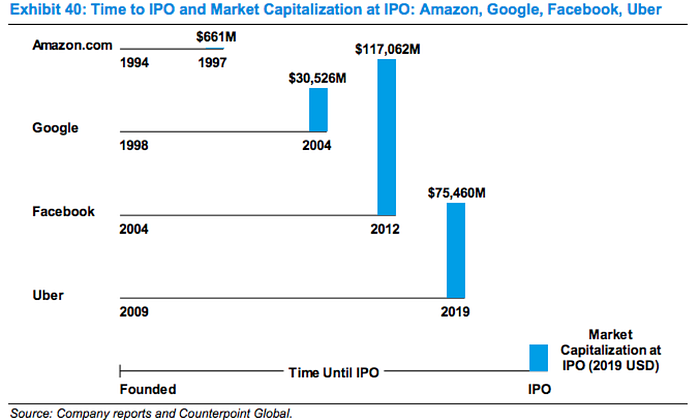

MS also looks at the time to IPO & Market Capitalization at IPO between AMZN, GOOGL, FB, and UBER. Amazon went public three years after it was founded with a market cap of $600M (in today’s dollars), Google went public six years after it was founded with a market cap of $30.5B, Facebook 8 years after its founding with a market cap of $117B, and Uber 10 years after its founding with a market cap of $75B. As companies have stayed private longer we’ve seen the re-emergence of crossover funds or “lifecycle investors”, such as Altimeter that care less about whether a company is public / private and more about the key attributes of the investment. There are a number of hedge funds with active private arms such as Adage, Coatue, D1, Lone Pine, Tiger, Viking, and Whalerock. Hedge funds always had a more opportunistic mandate than mutual funds / larger asset management complexes.

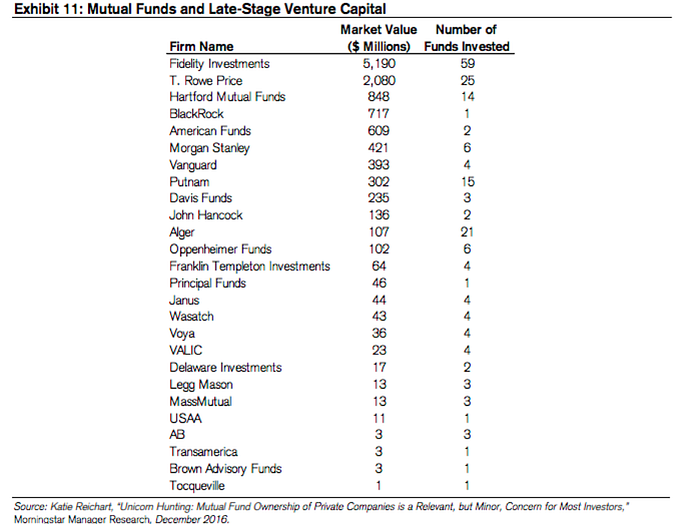

While the information below is a bit dated you can see this crossover phenomenon isn’t limited to just hedge funds but has active participation from the mutual fund community as they’ve been left out of the typical growth of a company from $500M-$10B+ which is where they historically were able to utilize a capital duration arbitrage to outperform broader market indices.

As funds begin to invest in both public & private markets this starts to “blur the line” of the clearly delineated boxes that institutional LP’s have slotted their managers in; providing managers flexibility to be “investors” first and foremost.

Public Market Risk Appetite

It’s tough to analyze growth equities in a vacuum without considering the macro backdrop, which we also discussed in Capital Allocation & Risk Asset Ramifications in a 0% Interest Rate World. That said as a result of the lack of IPO’s, and need to deploy capital there has been strong public market receptivity to IPO’s.

Market research firm Renaissance Capital published their “Fall 2020 IPO Preview” report in early September and noted that:

· In 2020, IPO’s have averaged a 36% first-day pop

· The Renaissance IPO index had returned 50% YTD (as of 9/4/20)

· Summer 2020 filings were up 50% from Summer ’19.

This was before the latest batch of IPO’s which included SNOW (+111.6%), JFROG (+47.3%), Unity (+31.4%), and SUMO (+22.2%), as well as Direct Listings such as ASAN (+37.1%), and PLTR (+31.0%).

It’s not just the IPO market where investors are rewarding the prospect of future growth. We’ve written at length about the Bessemer Emerging Cloud Index most prominently here. The index is +80.3% YTD, versus the NASDAQ +28.8%, the S&P 500 +6.9%, and the DOW (-1.3%). This has occurred as investors put a premium on recurring revenue, growth rates, and predictability of growth with top SaaS companies like DDOG, ZOOM, SHOP, and NET trading at 60.0x, 57.0x, 45.0x, and 43.5x annualized revenue, and 45.0x, 50.5x, 40.0x, and 33.5x NTM EV/S. While this screens rich on any traditional “value” metric public markets investors aren’t viewing these investments over a 6–12-month time horizon but are attempting to discount the future value of the cash flows over a 3,5, or 10-year period of time.

There’s been a lot of discussion YTD about “growth” vs. “value” and whether or not “value investing is dead.” Joel Greenblatt was recently on Barry Riholtz Masters in Business Podcast where he discussed the different definitions of value; excerpted below:

“It really depends on how you define value. If you define it like Russell or Morningstar where it’s low price book, low price sales investing, it’s had a tough time, an — an extraordinary time.

Last five years, growth — the way they define it at Morningstar or Russell — has outperformed value by 11 percent per year. Last three years, it’s 17 percent per year growth outperforming value. The last 12 months, it’s about 43 percent. These are phenomenal numbers. These are numbers bigger than during the five years before the top of the Internet bubble. These are slightly bigger, slightly bigger to discrepancy between growth and value.

So your question is — is very good. If you define value like we do, which is figure out what a business is worth and pay a lot less, that’s what I define as value investing. And, you know, Ben Graham would say leave a large margin of safety, then that’s never really going to go out of style. We — we look at companies like we’re a private equity firm. No private equity firm buys a business because it’s a low price book or little price sales. They’re really looking at cash flows.

So while in a period like this where anything that’s somewhat out of favor, even though it’s not low price book, low price sales, they rhyme together. And if people are willing to pay growth at any price, then that’s not going to be a good period for any style of value investing.

But if — and the question is is value investing dead or is it going to continue, it comes down to how you define it. And people will always come back to valuation. It’s based on cash flows and how much those cash flows are going to grow over time. As Buffett would always say, growth and value were tied at the hip. They’re part of the same equation, figuring out value. So once again, we’re talking about definitions.”

This is an incredibly important delineation because it’s this mindset that’s really starting to permeate across both public & private markets; value is buying something at a discount to what you believe it will be worth in the future and paying a lot less for it.

If you’re a Seed or Series A venture investor, investing in a company at a $5-$10-$25M-$30M valuation with limited revenue that doesn’t typically check the “value box.” But if you’re convinced that over the next 3–5–7–10 years the business has the potential to be a multi-billion-dollar company; that’s the definition of margin of safety. Your downside is 1 (or often times less given structuring and the ability to sell businesses) while your upside is 30–200x+ your initial capital. Similarly, buying ZM at $60/sh last October at 30.0x NTM EV/S could hardly be considered “value” investing, but when revenue is growing at 355%+, it sure looks like there was a “sufficient margin of safety” even if you had assumed multiple compression as opposed to the expansion we’ve seen due to macro factors outside of ZM’s control.

As public market investors are willing to have a more long-term outlook this is having ripple effects on all companies, including those that IPO’d 60+ years ago such as Disney. Activist investor Dan Loeb recently wrote a letter to DIS management team urging them to accelerate the Disney+ DTC offering and suspend their $3.0B/year annual dividend, redirecting it to content production. Academically trained “value investors” would never recommend the suspension of a dividend in favor of an investment with an uncertain NPV as it pertains to value accrual. But a mere five days after the letter was issued Disney announced a strategic reorganization of its media & entertainment business to “further accelerate the DTC strategy due to the rapid success of Disney+.”

The market reacted positively to the DIS news sending the stock +3.2% despite the lack of any really concrete action yet. NFLX spent ~$15B on content in 2019 & since 2015 NFLX has increased its annual content budget by an average of 34%/year, yet the stock is up ~400% over that time period. AMZN reportedly spends $6B/year on content and AAPL has apparently increased their content budget from $1B to $6B. This move by DIS would put them in-line with more highly capitalized competitors. Of course DIS has a rich content library from which to start with including Disney live action and Walt Disney Animation Studios, Pixar Animation Studios, Marvel Studios, Lucasfilm, 20th Century Studios and Searchlight Pictures.

Loeb too quoted Warren Buffett saying, “companies get the shareholders they deserve” and went on to say, “Disney deserves growth-minded, long-term oriented investors, & we believe that a strategy centered around using Disney’s many resources to drive growth in the DTC business will further attract them.” It’s this vantage point that has allowed Jeff Bezos to run AMZN the way he has for the past two decades, and why companies like SHOP, SQ, and TSLA defy any semblance of normalcy from a traditional valuation standpoint. They have earned enough respect from market participants that their core shareholders believe in the vision not for the next quarterly earnings print, or 12 months, but what they intend to do over the next 5–10 years.

Loeb wrote that Third Point has observed “numerous precedents of successful non-linear business model transitions that paid off handsomely for shareholders. Among such business transformations, Adobe and Microsoft stand out as particularly relevant examples of companies which, in order to optimize their distribution models, had to forgo lucrative upfront license revenues in exchange for monthly subscriptions. Investors have learned that while these strategic shifts may depress near-term earnings, their patience will be rewarded with businesses many multiples the size of what they once were. Furthermore, the stocks were rewarded with significantly higher multiples reflecting the superior quality of their new recurring, subscription revenue streams (a significant improvement over their historic lumpy transactional model). Both companies’ shares have appreciated significantly since these transitions began.”

This type of multiple re-rating has become more common, allowing CEO’s to make decisions that benefit their stakeholders over the long run, and thus rewarding long-term oriented shareholders. This isn’t too dissimilar from the emotional rollercoasters that go along with any startup, the only difference is there isn’t a daily mark to market, and for the most part investors don’t have the ability and / or liquidity to sell; and therefore are rewarded for their long-term orientation.

SPACs

In July we wrote a piece entitled, Return of the SPAC, which we thought was near the peak euphoria for SPAC issuance as Bill Ackman raised a $4.0B vehicle with the potential to be $5-$7B in total. We went over SPAC mechanics, the history of SPAC’s, advantages / disadvantages vs. IPO’s, Direct Listings, and sales to PE / Strategics. Since that post there’s been much more active SPAC issuance from the traditional Venture community with Ribbit Capital raising a $600M vehicle, Mark Pincus & Reid Hoffman raising a $600M vehicle, Altimeter raising a $450M vehicle, FirstMark raising a $360M vehicle, and Lux Capital looking to raise $375M vehicle. Then of course Chamath Palihapitiya who started this wave announced his first 3 transactions with IPOA buying Virgin Galactic, IPOB OpenDoor, IPOC buying CloverHealth, and raised his next three vehicles IPOD, IPOE, and IPOF of $400M, $700M, and $1B respectively.

While some believe these SPAC’s are a sign of the top and of frothiness across capital markets (which has indeed been the case historically); we believe there are some structural changes going on which may be here to stay. Prior to the Virgin Galactic / DraftKings SPAC deals there was a lack of historical precedent of a venture-backed company that could have IPO’ed and chose the SPAC path. SPAC’s were historically seen as a payment scheme for lower quality private equity sponsors. This resulted in limited interest from broader market participants. Merger Arbitrage funds were typically the biggest buyers of SPAC’s looking at them as alternatives to cash management vehicles, and ideally finding a way to sell the stock and the warrants on deal announcement looking to generate a 5–15% IRR. As we’ve seen higher quality sponsors and companies that would have found strong support in the IPO market you are starting to slowly see long only participation. They started their foray into the SPAC world by first getting active in PIPE’s that were raised as part of the deal announcement, but now they are moving “downstream” and have begun participating at the IPO stage (taking some “blind pool risk”) to get the “first look” at the PIPE as well as generate returns on the cash / warrants ahead of deal announcement. Each subsequent success is another case study / data point for late stage founders / CEO’s. SPAC’s allow companies to provide forward guidance which makes it a particularly attractive alternative for growth stocks.

We’re still in the early days of observing top quality companies / sponsors come to market via the SPAC route, but believe this combination coupled with structural modifications as it pertains to incentive fees, promotes, and warrant coverage mean that SPAC’s for growth companies could be here to stay.

This too leads to a blurring of public / private rounds. If companies can attract SPAC capital earlier in their life cycle do crossover funds start participating earlier? Do you see a migration of firms that participated in the PIPE, and then the IPO, ultimately look to participate in growth venture? If these companies continue to trade well does that embolden other venture backed companies to go public earlier than they previously would have whether via a SPAC, IPO or Direct Listing? What happens to venture valuations if you have “comps” that are of similar age, size, and scale that are public?

Liquidity Solutions

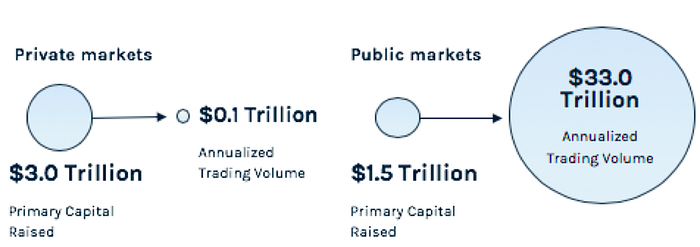

In our post entitled the Financialization of Everything, we highlighted that in 2015 private market capital raising surpassed public market capital raising for the first time, and it’s now nearly double on an annual basis, despite significantly more capital chasing public market opportunities than there were 5,10, 15 years ago. We also cited Tribe Capital’s work which showed public market trading volume is ~330x that of private markets yet, private markets raised 2x the amount of capital.

There are numerous FinTech firms that are looking to solve the liquidity need for private company shares including SharesPost, Forge, EquityZen, Carta, and NASDAQ Private Markets. There was initially some reticence amongst the VC community & founders to allow for any semblance of “public” price discovery. However, those companies that have been private for a number of years are looking for ways to help early stage employees find partial liquidity, while some early stage funds are also looking for liquidity to show returns to LP’s for subsequent fundraises.

As “founder secondaries” have become both more common & accepted and greater quantums of capital are competing for late stage venture exposure, this provides an opportunity for a more seamless secondary market of private company shares; with broader market acceptance from founders & venture capitalists alike.

These venues have historically run Dutch auctions as liquidity programs. We believe that as secondary’s become more common you start to slowly see the electronification of this market with RFQ’s and potentially even central limit order books; which again starts to look more and more like the public market.

Investment Criteria

One of the interesting things about the plethora of SPAC filings is going through the various S1’s and figuring out what criteria the sponsors are looking for in a potential investment.

If we look at the Pershing Square Tontine Holdings S1, Bill Ackman and team will “consider companies in a wide range of industries, but generally will seek to acquire a simple, high-quality, high-return on capital business that generates predictable growing cash flows that can be estimated within a reasonable range over the long term. [They] will prefer targets that have low sensitivity to macroeconomic factors, with minimal commodity exposure and/or cyclical risk.” They outline several acquisition criteria including:

· Simple, predictable, and free-cash-flow generative.

· Formidable barriers to entry

· Limited exposure to extrinsic factors that we cannot control

· Strong balance sheet

· Minimal capital market dependency

· Large capitalization

· Attractive valuation

· Exceptional management and governance

If we look at the IPOD-F series of S1’s Chamath & team have identified acquisition criteria including:

· are in the technology industry and can benefit from the extensive networks and insights [they] have built. In addition, [they] expect to evaluate targets in related industries that can use technology to drive meaningful operational improvements and efficiency gains, or enhance their strategic positions by using technology solutions to differentiate offerings;

· are ready to operate in the scrutiny of public markets, with strong management, corporate governance and reporting policies in place;

· will likely be well received by public investors and are expected to have good access to the public capital markets;

· are at an inflection point, such as those requiring additional management expertise, innovation to develop new products or services, improvement of financial performance or growth through a business combination;

· have significant embedded and/or underexploited expansion opportunities;

· exhibit unrecognized value or other characteristics that [they] believe have been misevaluated by the market based on [their] company-specific analysis and due diligence review. For a potential target company, this process will include, among other things, a review and analysis of the company’s capital structure, quality of earnings, potential for operational improvements, corporate governance, customers, material contracts, and industry background and trends; and

· will offer attractive risk-adjusted equity returns for [their] shareholders. Financial returns will be evaluated based on (1) the potential for organic growth in cash flows, (2) the ability to accelerate growth, including through the opportunity for follow-on acquisitions and (3) the prospects for creating value through other value creation initiatives. Potential upside from growth in the target business’ earnings and an improved capital structure will be weighed against any identified downside risks.

The Altimeter Growth Corp S1 identifies acquisition criteria including:

· Large and growing total addressable market. Based on [their] experience at Altimeter, [they] will prioritize [their] focus on investments in large and growing industries. These industries are ripe for new entrants to make significant share gains in winner take all or winner take most environment.

· Differentiated architecture. Effective architecture differentiation, along with the ability to continuously innovate are key to continue to acquire customers, grow sales, and deepen competitive moats. [They] will focus on companies that solve real business problems, including data analytics and enabling the shift to cloud computing.

· Multi- year “compounders.” [They] will aim to invest in a company that can deliver sustainable top-line growth for the long-term. [They] believe that the majority of the value creation will come from fundamental growth rather than financial engineering.

· Favorable unit economics. [Their] experience has taught [them] that not all growth is created equal. Strong unit economics are necessary to achieve sustainable growth over time and a path to high margin profitability in the long-term.

· Strong management team. [They] will look to partner with world class management teams who are capable of scaling a business around the globe. [They] will also evaluate ways to support and advance the team over time as needed.

· Sensible valuation. [They] have a deep understanding of both private and public market valuations and will aim to invest on terms that will provide significant upside potential while limiting downside risk.

The Ribbit LEAP S1 lays out the following acquisition criteria:

· World-class management teams. [They] seek management teams with whom [they] would be proud to partner for the next decade or more and who have the vision, energy, and execution capability to deliver on [their] high expectations for growth and franchise value. This is the standard against which Ribbit Capital measures all of the management teams it partners with, whether they are running public or private companies.

· Large addressable markets with attractive tailwinds for digital innovators. Financial services profits are large enough in the regions where Ribbit Capital invests to potentially support market capitalizations in the tens or hundreds of billions of dollars for market leaders. Furthermore, across sectors and regions, [they] see the opportunity for technology to make financial products and services more affordable and accessible for customers. [They] seek businesses that address these markets.

· User adoption suggesting a generational brand is being built. [They] believe that every new generation of users presents an opportunity to create a defining brand that stretches across multiple sectors within financial services. [They] seek businesses that show enough traction among their customers where [they] can see the potential for them to become generational brands.

· Significant growth opportunities. In addition to strong organic growth potential, [they] seek businesses that could meaningfully accelerate growth through new product and technological expertise, business combinations, geographic expansion, and/or a shareholder base that is aligned to long-term growth. [They] seek businesses for which [their] capital can fuel this development and growth.

· Strong unit economics and profitability visibility. In order to deliver enduring value creation for shareholders, [they] believe that a business must be profitable or on a clear and easily understood path towards profitability, which is most clearly demonstrated by unit economics that are attractive today.

If you look across each of those S1’s you notice a number of common themes including large end-markets, exceptional management teams, strong unit economics, significant growth opportunities, at sensible valuations.

This doesn’t sound all that different from Berkshire / Buffett’s investment criteria where he outlines:

· Large purchases (at least $75 million of pre-tax earnings unless the business will fit into one of our existing units),

· Demonstrated consistent earning power (future projections are of no interest to us, nor are “turnaround” situations),

· Businesses earning good returns on equity while employing little or no debt,

· Management in place (we can’t supply it),

· Simple businesses (if there’s lots of technology, we won’t understand it),

· An offering price (we don’t want to waste our time or that of the seller by talking, even preliminary, about a transaction when price is unknown).

It also looks similar to the playbook that Don Valentine at the complete opposite end of the spectrum as the “grandfather of Silicon Valley venture capital” focused on including:

· High gross margin & cash flow

· Back Companies in huge end markets

· Outside of product + marketing / sales, keep burn low

· Watch the G&A line like a hawk

Whether you are Warren Buffet buying businesses for a target hold period of “forever”, a public hedge fund manager like Bill Ackman, a crossover fund manager like Brad Gerstner, an opportunistic investor like Chamath Palihapitiya, or a VC trying to follow in the footsteps of Don Valentine, the core tenants of what constitutes a “good” investment are incredibly similar. As liquidity paradigms begin to change, market participants merge, and key business characteristics are valued comparably in public & private markets, the line between the two becomes less clear; and those who are able to identify & take advantage of those merging trends should outperform.